Investing doesn’t have to be hard.

Investing doesn’t have to be hard.

It should be fun.

And the end result should be a reward for the effort, discipline, and commitment to the journey.

But most investors make it hard for themselves.

Too hard.

It doesn’t have to be though… nor should it be.

Yet I see it time and time again in the market.

Now, I’m not perfect. No investor is. But if you understand the most basic fundamentals of investing, and actually put them into practice, then hard disappears, and fun becomes the name of the game.

I bring all this up this week because markets are in turmoil… yet again.

Let me show you a chart or two…

Do you notice any commonalities between these two charts?

Yeah, it’s clear enough: the price of both gold and silver have been parabolic for the last several months.

The thing is, parabolic usually isn’t a good sign. Not in gold, silver, Bitcoin, stocks… whatever.

Parabolic without rhyme or reason ends only one way.

You can ride it up, take advantage of it, get some quick fire profits, but always protect the downside.

Anyway, point being, I’m writing to you because markets are flat-out-bonkers. Volatility is wild across all assets. And that brings sharp, fast-moving risk. Moves can happen so quickly that you may need to act before we can issue an alert.

That’s why it’s important you read this in full.

Because with volatility comes a wide variation in outcomes.

What do I mean by that?

Think about it this way…

Had you invested in stocks in April 2025, by November you’d have thought you were the world’s greatest investor. But at that time… everyone was.

Had you invested in late October/early November, as of now, you’re probably ready to just throw the whole damn portfolio in the bin.

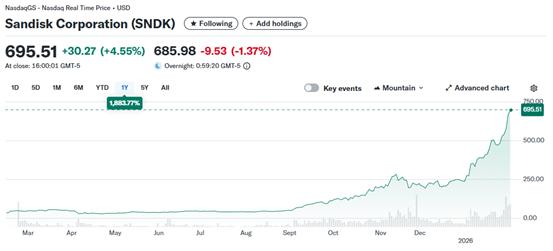

There are of course outliers to all this too. You look at a stock like Oracle, centre to the roll out of AI factories, and they’ve lost 50% of their value since October.

Meanwhile you look at a stock like SanDisk, also central to the rollout of AI factories and AI computing, and they’re up 1,883% in a year.

If you hold Oracle, you might hate the AI rollout about now.

If you hold SanDisk, you would bloody love it.

If you hold both, you’re still quids in because of the oversized outcomes of SanDisk, so you can wear a 50% haircut on Oracle.

This isn’t about praising one or burying the other. It’s to highlight that volatility is immense right now, and that risk comes in all shapes and sizes.

How your own portfolio is built will affect the outcomes you’re looking for.

It’s that element of risk in EVERYTHING you invest in that should always be primarily in an investor’s mind.

Because in my experience in the stock market for over 30 years now and in crypto markets for over 15, I can tell you that most investors think they understand their risk tolerance. In reality, they’re nowhere near able to stomach the risk their portfolio carries.

Furthermore, most investors do not manage their capital allocations in line with their risk tolerances, nor the risk of each position they choose to invest in.

You never really know your true tolerance until you’ve done your dough on a position.

Only then do you really know if you like risk or hate it.

Now, I’m not saying intentionally go out and try to lose it all on something highly speculative.

But if you’re investing in highly speculative, volatile, and risky assets – and yes, that includes everything I’ve mentioned above – then you absolutely need to be smart about how you allocate your capital and be prepared to be wrong.

Risk is everywhere in the market now, even the “safe haven” of gold. So do not think you’re immune to the prices of an investment going down, it happens in everything.

That applies to every single recommendation in every single service that we publish here at Southbank Research.

There’s not a single investment that’s published that doesn’t carry risk. And it also varies from reader to reader.

If you’ve been with us since 2016 and followed a recommendation like Bitcoin that we made in December 2016, then you’d be up roughly 10,000% on that (at today’s prices).

But if you’d joined us in November 2025 and decided to buy Bitcoin from something we’d published then, you’d be down roughly 25% and think it was the worst thing in the world.

It’s why you simply must take every investment much on its own individual merits…

And you might be the person that’s sufficiently resourced to punt $10,000 on a single stock, without fear nor care in the world if it were to go to zero. Your risk appetite would be up there to take on just about anything we publish.

But you might also be the person that’s sufficiently resourced to punt $10,000 on a single stock, but the prospect of that even turning into $8,000 puts the absolute fear of God into you.

Capital does not always equal risk tolerance.

And vice versa, I’ve known some of the most risk tolerant people have some of the least amount of capital to play with. They’re willing to take on a massive asymmetric risk play, with the view to turning $1,000 into $10,000 and then swinging for the fences again. But equally prepared that it tanks, and then they just start again later on.

This is also why, at Southbank Research, we present the risks in every recommendation but we never tell you how much to invest in a stock, even as a guide.

There’s no blanket rule that fits thousands of readers. And there’s no practical way that we can tell thousands of people to invest 1% or 10% or 100% of their capital into any given investment.

Which is why typically we’ve always stayed away from portfolio allocations. We present the research, the risks, the action to take and then the decision to buy, or not to buy, is in your hands.

It is again very much, each to their own.

Now, if you don’t understand portfolio allocation…If you don’t know how to judge your real risk tolerance…If you’re not comfortable with the fact that investments swing up and down — and that there are no guarantees in markets —

Then you may need to start with the basics first.

We will be putting together more material on the foundations of investing. But until then, it’s critical that you read everything we send you so you fully understand the positions, the risks, and what you’re actually buying.

I have a sneaking suspicion not everyone does that.

And that brings me to the headline of this essay…

How to Become a Great Investor in Two Simple Steps

I recommend a simple approach to risk and investing. Anyone can follow it.

In fact, it’s so straightforward that some have said it’s simplistic (childish even) and obvious. But that’s fine by me. Given the choice between making the same money the hard way or the easy way, I’ll take the easy way every time.

But that doesn’t mean being lazy. It just means that you’re not making things more complex than they should be.

So, I make no apology for keeping things simple. To be honest, I’d say our approach is so simple you could teach it to your kids or grandkids.

But before you teach anyone else, let’s start with you.

Step 1: Don’t be a lazy investor — use compartments

I’ll be straight up. I know this will go against everything you thought you knew about investing, but the fact is, I don’t like diversified investments.

I see diversification as a bit disappointing. I take the view that real market success comes from concentration and conviction.

But I’m also wildly risk tolerant. What works for me will terrify others.

This is important to lay as a foundation, that each of us invests differently. And that’s a good thing.

But even with how I approach risk and investing. There is a step which I think helps all investors.

That’s compartmentalisation.

What do I mean by that?

I think lazy investing rots a portfolio. It involves sticking money in a broad range of investments and then not paying much attention to how those investments perform.

Financial advisers might call this the “set and forget” approach.

Oh my days I hate that phrase.

It’s the epitome of lazy investing. If you won’t engage with your hard earned money, why earn it at all?

Lazy investing also means not fully reading, understanding and considering the implications of the investments you make.

Don’t be lazy!

Compartmentalising your investments is an active way of making a decision about where you’ll invest. In short, it’s not a scattergun approach, it’s not set and forget, it’s getting involved in “the trenches” and giving a damn.. It’s also a well thought out and executed approach.

Let’s show you an example of what I mean…

Your first step might be to split your liquid and investable assets into two blocks. I call one block ‘Sleep at Night Money’ and the other block ‘Punting Money’.

Remember, this is just a suggestion to get you on the right path to investing. You may come up with a different way to compartmentalise your money and assets that better suits you. Or you may just use one of these compartments, not both.

I’m not telling you, ‘This is how you must do it’. This is about getting you to think more about how you manage your money and risk.

In the ‘Sleep at Night Money’ block, you should include your long-term investments. This might be your gold, metals, bitcoin and dividend-paying stocks. And just because it’s “Sleep at Night Money” doesn’t mean you ignore it.

If a stock you’ve bought doesn’t appear to be living up to expectations, sell it. If you’ve tripled your gold holding value, take some profit. Cut losses, ride winners up and protect your backside, clip profits, invest smart.

Things change. Markets swing. Black Swan events happen and will happen in the future. So always remember that if you feel uncomfortable about something then maybe you shouldn’t be doing it.

If you’re uncomfortable with a position down 30%, sell it — even if we still hold it.Likewise, if a position is 400% up, you can take some profits if that helps you run it higher. Even if we haven’t issued a take profit alert.

We are guides, but you are the one that walks your own trail. And being an independent, free thinking investor is really the name of the game.

In the ‘Punting Money’ block, would be your speculative investments. Small and microcap pre-revenue growth stocks, crypto, big thematic early stage of the bell curve stocks, out-of-the-money options, things that have a healthy asymmetric risk component.

And by asymmetric risk I mean, the concept of a small allocation of “risk capital” is needed to unlock the potential of outsized returns. So much so that if you only hit one or two winners, you can easily make up for and outperform any of the losers.

With these speculative plays, you might lose on four or five and then hit one that’s a 1,000% winner. That one winner puts you ahead and lets you reload to go again.

Sleep at night compartment, punting compartment.

It’s that simple.

Once you’ve done that, you’re already actually well on your way to step two.

Step 2: Sort your risk out

I’ve covered most of this already, but this really is the thing where most investors fall down and the whole experience of investing becomes a chore, painful, difficult and stressful.

If it’s stressful and difficult, I suggest you look for term deposits and known outcomes. Use an index fund or something that you can really just forget about.

But if you want to be active, not lazy and really invest where you can have fun, swing for the fences occasionally and get insight into the market where you probably wouldn’t typically look, then sort your risk out.

I know you may be reading this and hate the investments I cover and research. Things like crypto, like breakthrough technology stocks, like small and microcap plays that are highly speculative and risky. You might hate it because you find it’s far too risky, too speculative, or you just think I’m an idiot.

That’s fine. Don’t subscribe.

You might prefer the angle and insight from Jim Rickards and the team at Strategic Intelligence. You might prefer gold, and metals, and all of the “defensive” plays in the market.

That’s fine, great, subscribe there.

Either way, know that each side of the fence carries risk. Be it research from me, from James Altucher, Jim Rickards, Zach Scheidt, Dan Amoss, Chris Campbell or Chris Cimorelli, everything comes with a varying element of investment risk.

We’ve seen that in the charts from earlier. Regardless of the market, everything that all our editors cover carry risk.

And when you can accept that, ease yourself into it, embrace it and know deep down that you’re investing true to your capacity to deal with that risk then you will enjoy it.

There’s no formula for becoming a great investor. It takes time. Patience. Experience. But most of all, it takes self-awareness.

Desperation is a portfolio killer. Emotional trading is a portfolio killer. Not understanding your risk tolerances is a portfolio killer. Poorly allocating your capital after all that is a portfolio killer.

But if you’re calm, collected, rational, deeply understanding of your risk appetite — if you know what belongs in “Sleep at Night” and what belongs in “Punting” — investing is one of the most fun things in the world to do!

We wish investing didn’t have to be so involved. It would be great if you could just set money aside knowing for certain that you’ll be rich when it counts and generations to come will be set for life.

But wishing won’t get you far in this market…or in retirement. You have to be decisive and active and know that’s just not how markets, or life, works.

By following this simple two step approach you can do everything in your power to put yourself in the best position for success and importantly to enjoy it along the way.

Regards,

Sam Volkering

Investment Director, Southbank Investment Research

P.S. Just this week, the Alaska Beacon reported that the Trump administration is moving ahead with new federal oil and gas lease bids in Alaska’s Cook Inlet.

That’s not speculation. That’s action.

This is exactly the kind of policy shift Jim was anticipating — and why he decided to publicly name a stock tied to the Alaska North Slope development.

When planning turns into execution, the window can narrow quickly. If you haven’t yet watched Jim’s recent briefing, now would be the time to do it.